Negative Equity Auto Loan: Smart Strategies to Avoid Financial Pitfalls

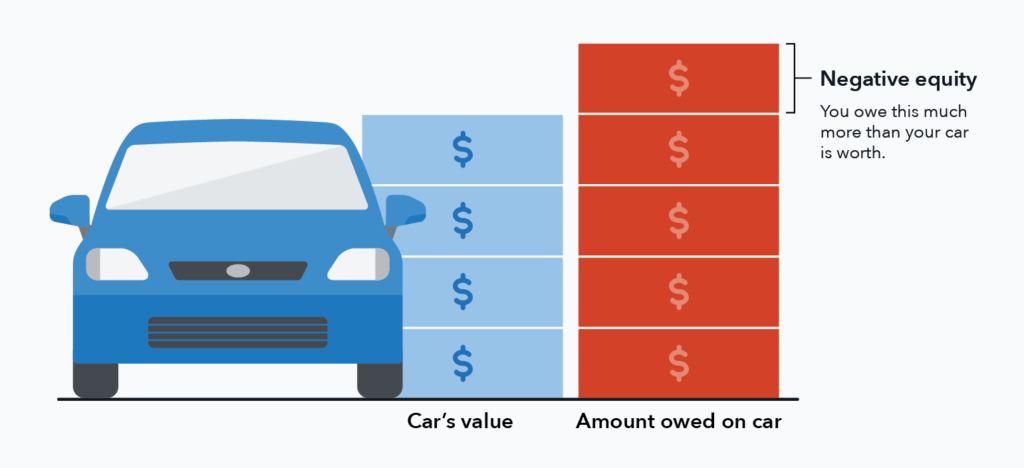

Are you stuck in a car loan that feels like a financial trap? If you owe more on your vehicle than it’s actually worth, you’re dealing with what’s called a negative equity auto loan.

This situation can make trading in your car or buying a new one feel overwhelming and confusing. But don’t worry—understanding negative equity and learning how to manage it can save you money and stress. You’ll discover practical steps to handle negative equity, options to protect yourself, and smart strategies to get back on track with your auto loan.

Keep reading to take control of your car finances and avoid common pitfalls that could cost you more down the road.

Negative Equity Basics

Local banks and credit unions in Austin offer good refinancing choices for auto loans. They often provide lower interest rates than big lenders. This can help reduce your monthly payments and total loan cost. Smaller institutions may also offer personalized service and flexible terms.

Benefits of lower interest rates include paying less money over time and faster loan payoff. Even a small rate drop can save hundreds of dollars. Lower rates improve your loan’s affordability and ease financial stress.

To refinance successfully, start by checking your credit score. Gather current loan details and vehicle information. Compare offers from several local banks and credit unions. Read terms carefully, focusing on fees and penalties. Apply with lenders that fit your needs and budget. Timely payments on the new loan will improve your credit over time.

Financial Risks Of Negative Equity

Negotiating with dealers can be tricky when negative equity is involved. Dealers might offer to roll the negative equity into your new loan. This means the amount you owe on your old car adds to your new loan balance. It can increase monthly payments and total interest paid. Always ask for a clear breakdown of costs before agreeing.

Consider these alternative trade-in strategies to avoid problems:

- Pay off the negative equity separately before trading in your car.

- Sell your old car privately to get a better price.

- Delay buying a new car until you have less or no negative equity.

These options help you avoid higher loan balances and better control your finances.

Frequently Asked Questions

Can You Get A Car Loan With Negative Equity?

Yes, you can get a car loan with negative equity. Lenders may roll the negative balance into the new loan. This increases your loan amount but allows you to finance a new vehicle despite owing more than your current car’s value.

Can I Trade In A Car With 10,000 Negative Equity?

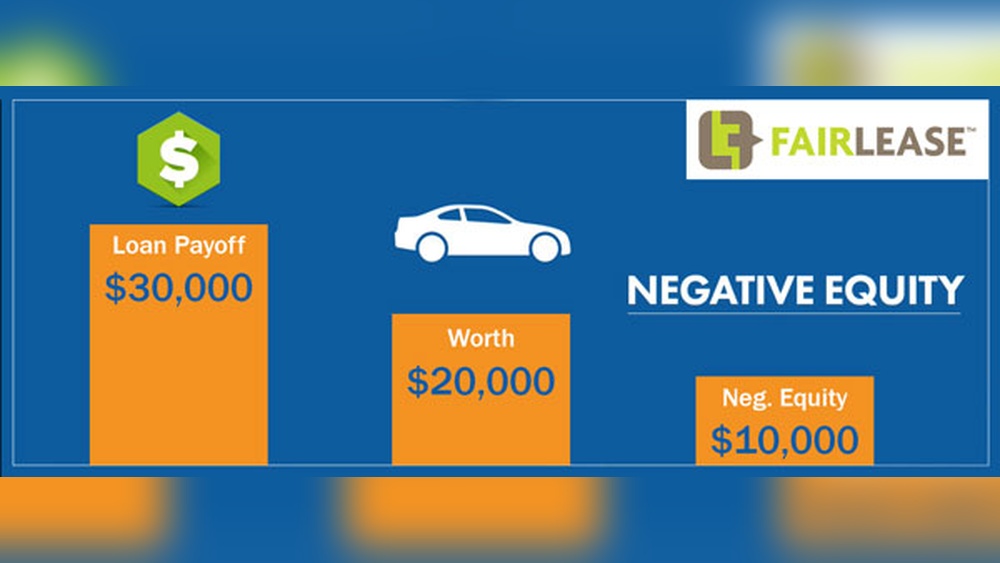

Yes, you can trade in a car with $10,000 negative equity. The remaining balance usually rolls into your new loan. This increases your new loan amount and monthly payments. Consider paying down the negative equity first or refinancing for better terms to avoid financial strain.

What Is The $3000 Rule For Cars?

The $3000 rule for cars suggests avoiding purchases over $3,000 above a vehicle’s market value to prevent negative equity. It helps buyers avoid owing more than the car is worth, reducing financial risk during resale or trade-in.

How Long Does It Take To Get Rid Of Negative Equity?

Getting rid of negative equity usually takes until the loan balance matches or drops below the car’s value. This can take months or years, depending on extra payments, refinancing, or simply waiting until the loan term ends. Paying down the principal faster speeds up the process.

Conclusion

Negative equity auto loans can feel like a heavy burden. Paying extra each month helps reduce what you owe. Refinancing may lower your payments and interest rates. Staying with your car until the loan ends also works. Gap insurance protects you if your car is totaled.

Knowing your car’s value is key before making decisions. Taking small steps can improve your financial situation over time. Managing negative equity requires patience but leads to financial relief.

Read More

- International Driving Permit Guide: Essential Tips for Global Travel

- Brake Replacement Cost Estimate: Save Big with These Expert Tips

- Electric Vehicle Battery Replacement: Cost, Tips, and Lifespan Guide

- Preventive Car Maintenance Checklist: Essential Tips for Longevity

- Commercial Driver Insurance Rates: How to Save Big in 2026

- Driver License Renewal Online: Quick, Easy, and Stress-Free Steps

- High Mileage Driver Insurance: Save Big with Smart Coverage Choices

- Winter Driving Safety Tips: Essential Strategies for Cold Roads

- Delivery Driver Insurance Coverage: Essential Protection Tips

- Balloon Payment Car Finance: Smart Tips to Save Big Today