Commercial Driver Insurance Rates: How to Save Big in 2026

If you’re a commercial driver, you already know how important insurance is for protecting your business and your livelihood. But have you ever wondered why commercial driver insurance rates can vary so much?

Understanding what affects your insurance costs can help you save money and get the coverage you need. You’ll discover the key factors that influence commercial driver insurance rates, tips to lower your premiums, and how to find the best deals tailored just for you.

Keep reading to take control of your insurance costs and keep your business moving forward with confidence.

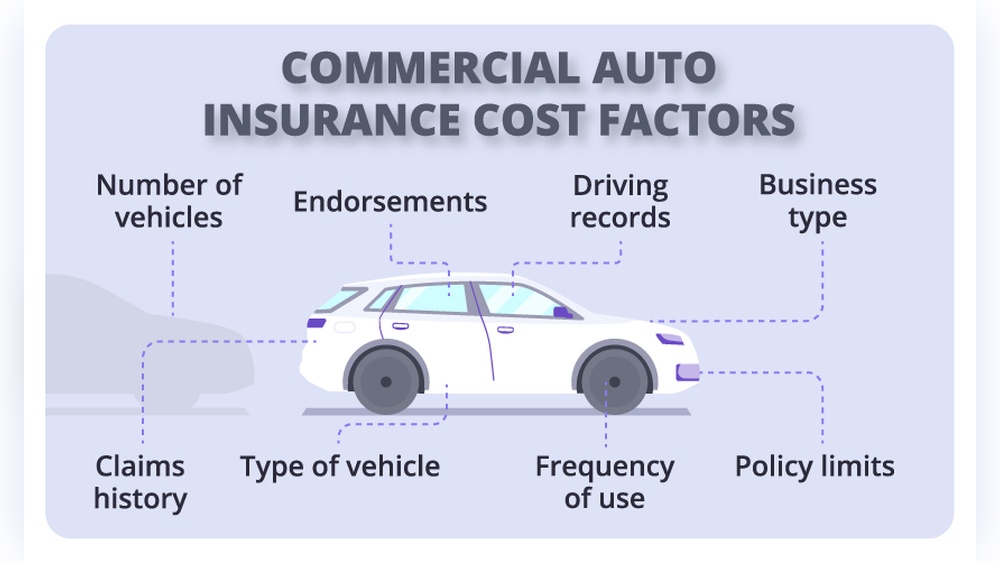

Factors Affecting Commercial Driver Insurance Rates

Vehicle type greatly affects insurance rates. Larger trucks or those carrying hazardous materials cost more to insure. How often and where you use your vehicle also matters. Vehicles used daily or for long hauls usually have higher rates.

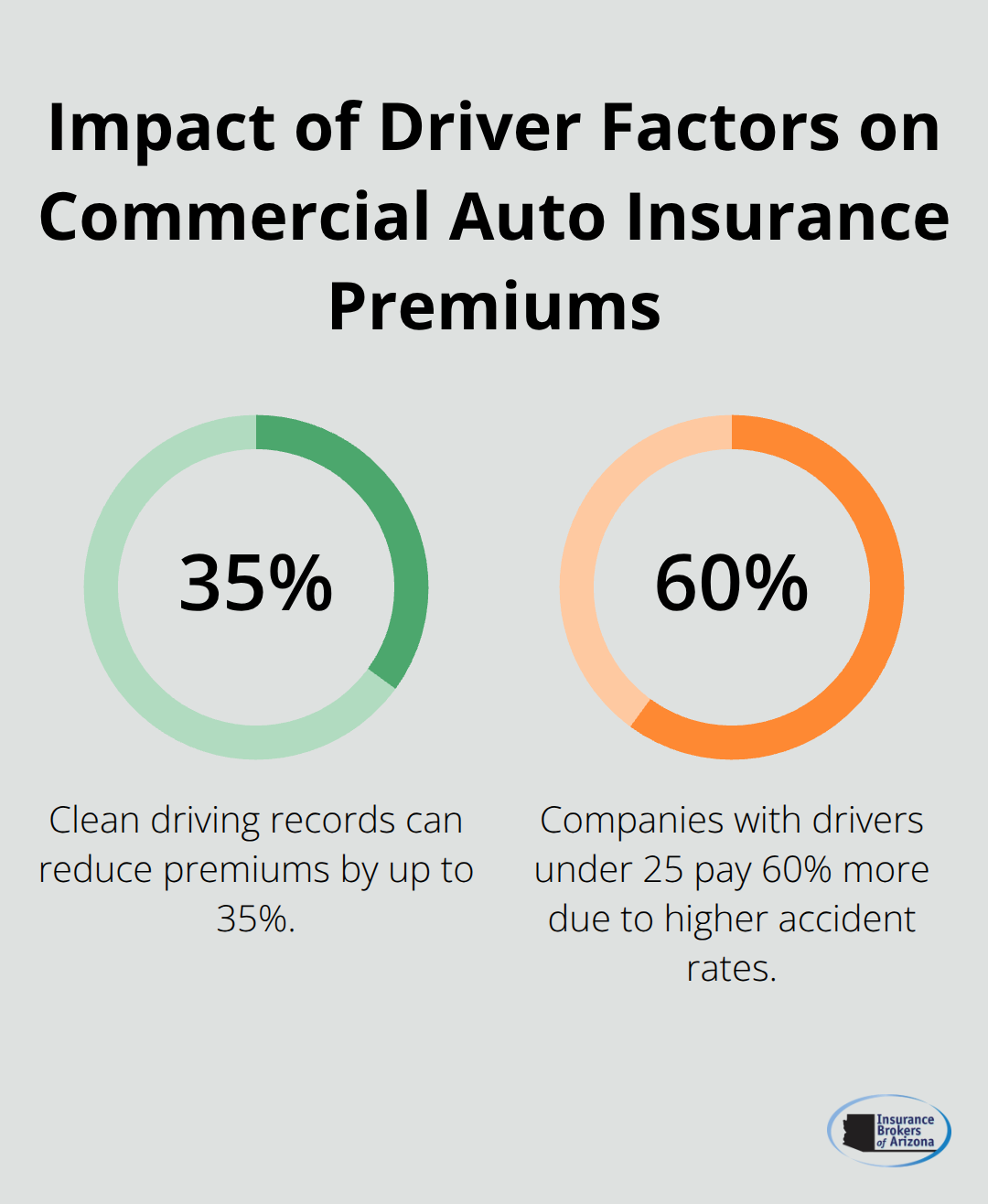

Driver experience plays a big role. Drivers with a Commercial Driver’s License (CDL) often get better rates. This license shows they have special skills and training. New or less experienced drivers may pay more.

Coverage levels and deductibles change the price too. Higher coverage means higher premiums. Choosing a bigger deductible can lower your cost but increases what you pay after a claim.

Some industries and routes carry more risk. For example, drivers in construction or hazardous goods transport pay more. Routes through busy cities or dangerous areas also raise rates.

Insurance costs vary by location. Urban areas usually have higher rates than rural ones. This is due to more traffic and theft risks.

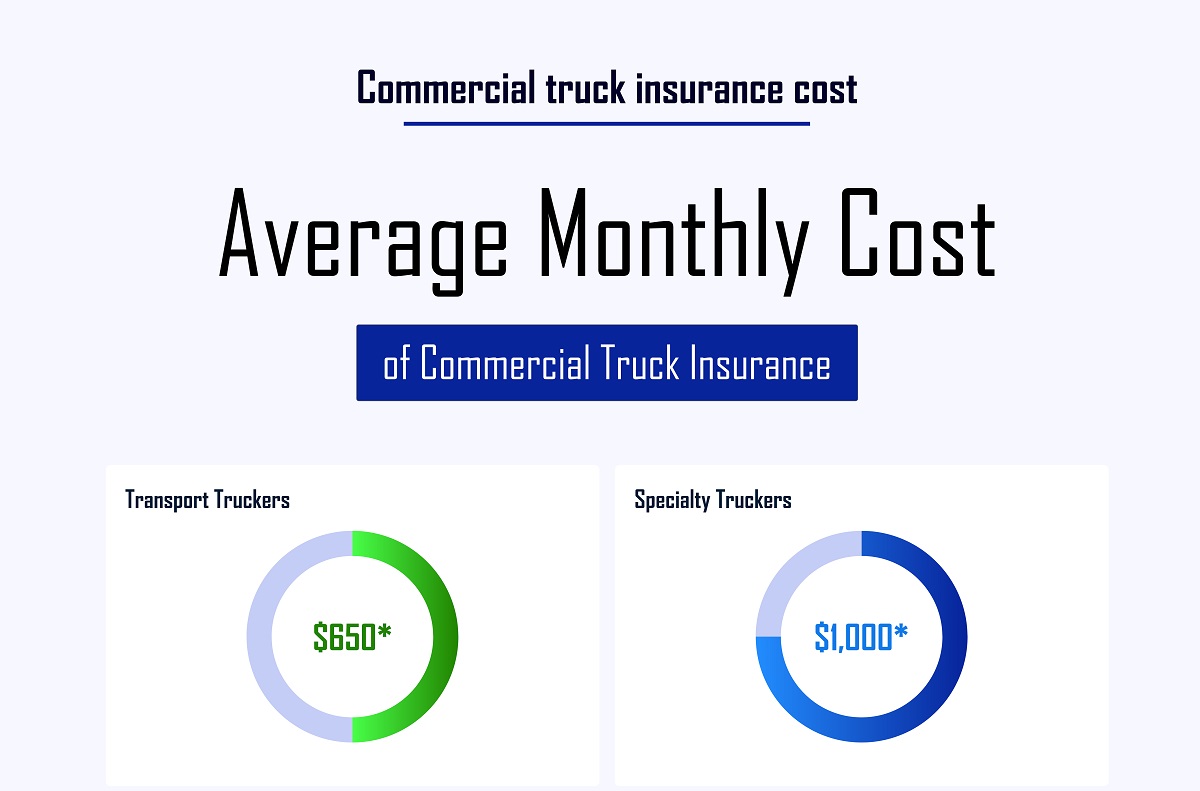

Typical Costs Of Commercial Driver Insurance In 2026

Average semi-truck insurance premiums in 2026 range from $6,000 to $12,000 per year. New businesses often pay higher rates due to lack of driving history. Established operators benefit from lower premiums thanks to proven safety records.

Rates can change a lot by state. For example, in Texas, costs are usually 5-10% lower than the national average. This is because Texas has many trucking companies and competitive insurance markets.

| Payment Option | Benefits | Considerations |

|---|---|---|

| Monthly | Smaller payments spread over time | May include extra fees or interest |

| Annual | Often cheaper overall cost | Requires larger upfront payment |

Strategies To Lower Insurance Premiums

Safe driving records help reduce insurance costs. Drivers with fewer accidents and tickets often pay less. Training programs improve skills and lower risks. Insurance companies reward careful drivers with better rates.

Choosing the right coverage matters. Avoid paying for unneeded extras. Select limits that fit your business size and risks. This keeps premiums manageable without losing protection.

Discounts and bundles cut costs. Combining policies or buying from one insurer often saves money. Ask about discounts for good credit, safety devices, or multiple vehicles.

Well-maintained vehicles lower claims chances. Regular checks, repairs, and servicing prevent breakdowns and accidents. Insurers see this as less risky and may lower premiums.

Telematics devices track driving habits. They report speed, braking, and routes to insurers. Safe driving shown through technology can earn discounts and better rates.

Insurance Providers And Comparison Tips

Top companies for commercial truck insurance include Progressive, GEICO, and State & Co. Each offers different coverage options and rates.

Check what each policy covers. Look for liability, collision, and cargo protection. Make sure it fits your business needs.

Use online quote tools to compare prices. Enter accurate details about your truck and driving record. This helps get better quotes.

Read the fine print carefully. Watch for exclusions, deductibles, and limits. Know what costs you may pay out of pocket.

Special Considerations For New Commercial Drivers

New commercial drivers often face higher initial insurance premiums. This is because insurers see them as higher risk due to limited driving history. Building a favorable insurance record helps lower these costs over time. Safe driving and no claims contribute positively to this.

Completing proper training and certification can reduce insurance rates. Certified drivers show insurers they have better skills and knowledge. This can make a difference in premium costs.

Owner-operators have unique insurance options. They can choose policies that cover both the vehicle and business liabilities. Comparing quotes from different providers helps find the best rates.

Impact Of Technology And Regulations On Rates

Advances in safety technology have helped lower insurance rates. Features like automatic braking, lane departure warnings, and collision avoidance systems reduce accidents. Fewer accidents mean fewer claims for insurers. This leads to lower premiums for commercial drivers.

Regulatory changes also impact insurance rates. New laws may require stricter driver training or higher safety standards for vehicles. Some regulations can increase costs, while others encourage safer driving, which lowers rates. Insurance companies adjust rates based on these rules.

Future trends include more use of data and telematics. This technology tracks driving habits and road conditions. Better data helps insurers offer fairer and more personalized rates. Also, electric and autonomous vehicles may change risk factors and insurance pricing in the coming years.

Frequently Asked Questions

How Much Does Commercial Vehicle Insurance Usually Cost?

Commercial vehicle insurance typically costs $1,200 to $5,000 annually. Rates depend on vehicle type, coverage, and driving history.

How Much Is A $1,000,000 General Liability Policy?

A $1,000,000 general liability policy typically costs between $400 and $1,500 annually. Rates vary by industry, location, and risk factors.

Do Commercial Drivers Get Cheaper Insurance?

Commercial drivers may get cheaper insurance if they have a clean driving record and a valid CDL. Discounts vary by insurer.

How Much Is Insurance On A $10,000 Engagement Ring?

Insurance on a $10,000 engagement ring typically costs 1-2% of its value annually. Expect to pay $100-$200 per year. Rates vary by provider and coverage options.

Conclusion

Commercial driver insurance rates vary based on many key factors. Your driving record, truck type, and coverage choices affect costs. Shopping around and comparing quotes helps find better deals. Maintaining a clean record can lower your premiums over time. Understanding these rates helps you plan your budget well.

Stay informed and review your policy regularly for savings. Insurance protects your business and keeps you moving safely.

Read More

- International Driving Permit Guide: Essential Tips for Global Travel

- Brake Replacement Cost Estimate: Save Big with These Expert Tips

- Electric Vehicle Battery Replacement: Cost, Tips, and Lifespan Guide

- Preventive Car Maintenance Checklist: Essential Tips for Longevity

- Driver License Renewal Online: Quick, Easy, and Stress-Free Steps

- High Mileage Driver Insurance: Save Big with Smart Coverage Choices

- Winter Driving Safety Tips: Essential Strategies for Cold Roads

- Delivery Driver Insurance Coverage: Essential Protection Tips

- Balloon Payment Car Finance: Smart Tips to Save Big Today

- Advanced Driving Lessons Cost: Ultimate Guide to Affordable Excellence